- Empire

- Posts

- 🐺 Feeding the wolf

🐺 Feeding the wolf

Taking stock of crypto's big narratives

David Canellis & Katherine Ross

February 10, 2025

Empire is coming to you live from the memecoin trenches.

Kanye West, during his most recent edge-lording session on X, said he’d declined to launch a coin because they “prey on fans.”

Meanwhile, Barstool Sports owner Dave Portnoy has embraced an unofficial coin of which he’d been sent supply, JAILSTOOL, and has been spending merch funds on buying even more of it.

This is crypto, where things are obviously very serious.

Elsewhere:

BTC has now been rangebound between $90,000 and ~$109,000 for nearly three months. Current price: $97,600.

BERA has settled at a $540 million market cap following last week’s launch, down 66% on its initial list price.

Over $1.3 billion net has flowed into Ethereum bridges in the past week, per DeFiLlama.

🐺 Wolves all the way down

There’s meant to be two warring wolves within all of us.

But in crypto, there’s so many more than two.

The story goes that whichever wolf we feed the most will grow strong and devour the other. It's a metaphor for good and evil — nurturing virtue in the soul will scrub it clean of all things fiendish, eventually.

So, which wolf is crypto feeding? Take your pick:

Permissionless finance and censorship resistance

Tokenization of all things

Memecoin casinos

Public goods funding

P2P cash

Wall Street adoption

DAOs and onchain governance

Regulated stablecoins and tokenized money market funds

Incentivizing physical infrastructure networks

Digital collectibles

Yield and airdrop farming

Mixers and privacy tech

Charity and scientific research

Crypto-powered smart cities

There’s likely many more that have slipped my mind. Still, what’s clear is this: crypto’s builder culture has conditioned us to believe that it’s possible — and optimal — for all wolves to be fed at the same time and not tear each other’s throat out in the process.

Take the alpha wolves of this particular cycle: Wall Street adoption and memecoin casinos.

Setting aside the potential for a Dogecoin ETF to bridge the gap between those two concepts, an exceedingly well-fed Wolf of Wall Street Adoption would be far more powerful than mere memecoins in TradFi wrappers on stock exchanges.

Perhaps its final form would involve tokenized stocks, bonds, foreign currencies and all other financial instruments trading round-the-clock on public blockchain rails — and globally accessible to boot.

Or it is hedge, mutual and pension funds making long-term investments far across the crypto space, rather than just buying and selling bitcoin for its volatility (or ill-timed investments in centralized lenders and exchanges).

At this moment, it’s difficult to imagine either scenario playing out — as much as I might like them to — because the Wolf of Memecoin Casinos is simply far too big right now.

Take the first facet of adoption: the fulfillment of Larry Fink’s vision of tokenization as the “next generation for markets.”

Wall Street has already burned through the idea of porting finance to permissioned blockchains. But public chains in their current form, especially ones that have pushed for a decent degree of decentralization, often barely withstand major influxes in activity before service degrades.

It’s happened on Ethereum, Solana, Base, XRPL and others when memecoins were broadly super hot, but more recently Solana infrastructure chugged solely around two big memecoins: TRUMP and MELANIA.

Maybe they’d use their own layer-2s or layer-3s, but essentially, Wall Street would want to adopt networks that can handle many, many more wildly popular assets all at once, and not have to compete against memecoin traders to use the chain.

As for the second — funds investing in crypto long-term like they do with stocks and bonds — they will no doubt base those decisions on fundamental metrics, like Blockworks Research’s Real Economic Value (REV), which points to memecoin trading as the prevailing avenue for accruing value in public blockchains right now — even if they can only handle so much of it.

Is investing in crypto infrastructure powering profitable onchain casinos enticing enough for old-world financial institutions? Maybe some.

I’d still bet more would jump if another one of crypto’s rabid wolves were properly fed.

— David

P.S. Help us build a better Empire and complete our short audience survey. Thank you!

Six weeks until DAS NYC.

Big names. Big conversations. Big moves.

Mohamed El-Erian on the macro forces shaping global markets.

Mike Novogratz on where institutional capital is actually flowing.

Anatoly Yakovenko on the tech pushing crypto and finance forward.

Bring your team. Group passes are 25% off for 10+ people, but only until Feb. 14. Smaller groups (4-9) still save 15%.

📅 March 18-20 | NYC

It’s not just Strategy: US endowments are eager for some bitcoin exposure.

Former Binance CEO Changpeng Zhao was critical of Binance’s token listing process, calling it a “bit broken” though he doesn’t have any solutions for it.

Don’t panic: Base is moving its sequencer fee earnings to Coinbase’s custody for “security” and “audit” reasons, according to a team member.

🙃 Mixed messages

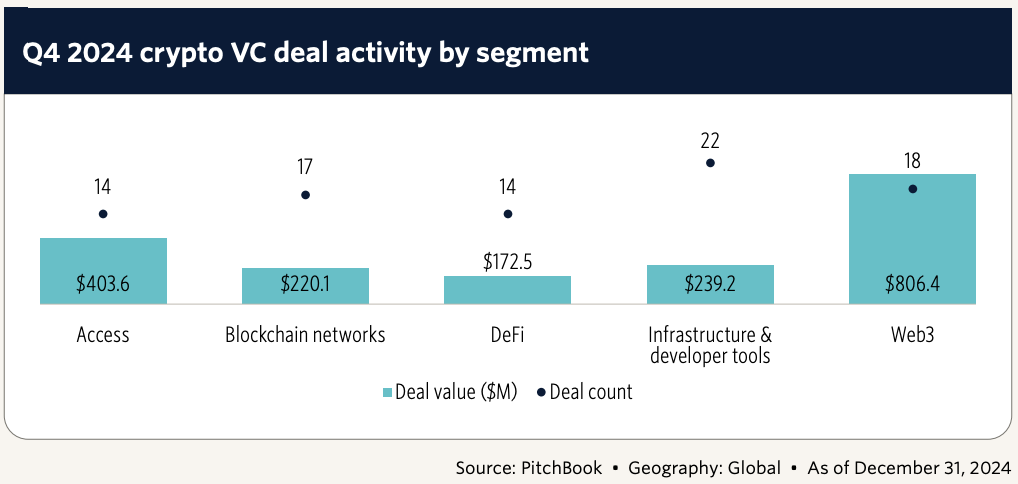

Crypto venture capital spending continued to stay on the lower end throughout the end of 2024, PitchBook found in a new report.

Breaking it down by the numbers: deal values jumped to $2.4 billion in the final quarter of 2024 — a 13.6% increase from the third quarter but the number of deals declined to 351 from 411.

A look at where the capital's going.

“While the rebound in funding suggests that investors remain willing to back established teams and differentiated technologies, the continued pullback in deal count highlights growing investor selectivity — a dynamic that first became evident in Q3,” PitchBook’s Robert Le wrote.

If you’re an optimist looking for the silver lining, this could mean that we’re seeing a concentration in fewer projects that show more promise. If you’re a pessimist, then the data plays into the narrative that we’re still not back to pre-crypto winter levels.

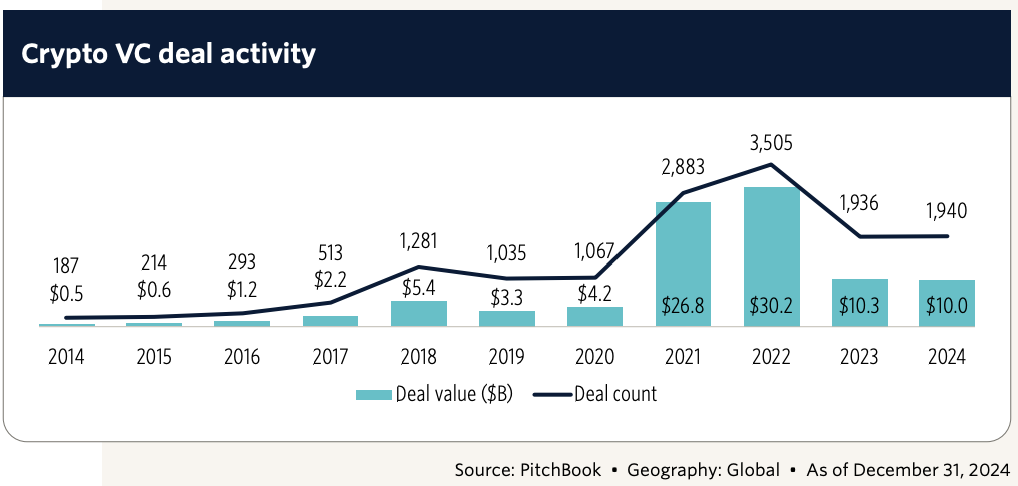

If we look at 2023 and 2024, the data is not so different.

Last year, crypto VC spending topped out at $10 billion across 1,940 deals. In 2023, investors deployed $10.3 billion via 1,936 deals.

Values, however, were on the rise in 2024 — another point to the optimists.

Still nowhere near the 2021 and 2022 cycles.

Let’s break it down a bit more: The median check cut in the seed stage jumped 20% to $3 million last year from $2.5 million. Then you have early-stage funding, which rose 26% to $4.8 million.

Late-stage, however, saw a slight drop from $6.4 million to $6.3 million, suggesting that “founders at more mature companies are raising smaller but strategically focused rounds rather than pursuing the larger checks seen in previous cycles” Le wrote.

We can pick apart the data to fit whatever narratives we want to see. But there’s no doubt that there are both positives and negatives. Don’t be surprised that crypto VC spending isn’t back to 2021 levels, and don’t expect that kind of comeback to happen overnight either.

On the other hand, the data perhaps shows some maturity happening in the crypto VC space.

That is, perhaps, a nice little break from the jailstool narrative.

— Katherine

On our mind: The invisible hand of the crypto market

Katherine: I’m not sold on an invisible hand. Narratives come and go — AI coins one week, VC coins the next. Crypto’s more of a go-with-the-flow kind of thing in my opinion. Now, if you asked me if there’s an invisible hand in the equity market…let’s not go there, I guess. But if you wanted a potential invisible hand I guess we could follow the money and make a case for VC investments, since they drive a lot of capital in the space (obviously). You can use it as a way to gauge how narratives are performing in a way, as I sometimes do. Does this mean you should be paying more attention to VC activity? To each their own. It’s a good read, but take it with a grain of salt, after all, I totally understand some of the criticism surrounding VC coins like Berachain. | David: The whole “many wolves” analogy hinges on the idea that the market makes collective decisions about where to invest. That’s obviously not the case. Stuff just comes out in the wash and sucks the air out of the room. NFTs did it, memecoins are doing it, and no doubt some other weird primitives will have the same effect over the coming years. Like Katherine, I’m not sure there’s so much of an invisible hand in the crypto market. It moves too quickly, with all the bleeding edge discourse playing out on social media and other channels. Influencers drive investment theses by posting publicly (just look at Yaps) and narratives are reinforced when the market jumps. Maybe the “visible mouth of the crypto market” is more appropriate. |