- Empire

- Posts

- 🌊 Buy high, sell low

🌊 Buy high, sell low

Almost every ETH ETF is underwater right now

David Canellis & Katherine Ross

February 13, 2025

If crypto market cycles had Four Horsemen like the Apocalypse, then maybe Joe Lubin would be one of them.

Lubin this morning jumped in to defend Vitalik’s “make communism great again” post on X, which was tongue-in-cheek but still riled some corners of the ETH space, especially those who think the Ethereum Foundation has lost its way by prioritizing public goods over profitable apps.

Curiously, the Consensys founder reckons we’ve never really experienced “capitalism on planet Earth,” which is exactly what proponents usually say about communism. Welcome to the upside down!

Otherwise:

BTC is almost exactly where it was yesterday at a touch under $95,900.

BNB has flipped SOL after rising 20% in a week, pushed up by a round of promos on CZ’s X timeline.

Under 19,000 active addresses were recorded on Berachain on Wednesday, down from almost 1.2 million at its peak on Tuesday, per Blockworks Research data.

🫂 Just like us

There’s endless shared trauma in crypto. But among the most common feels would be the kick to the guts that is buying a coin only to have it crash almost immediately.

Buyers of ETH ETFs are going through it right now.

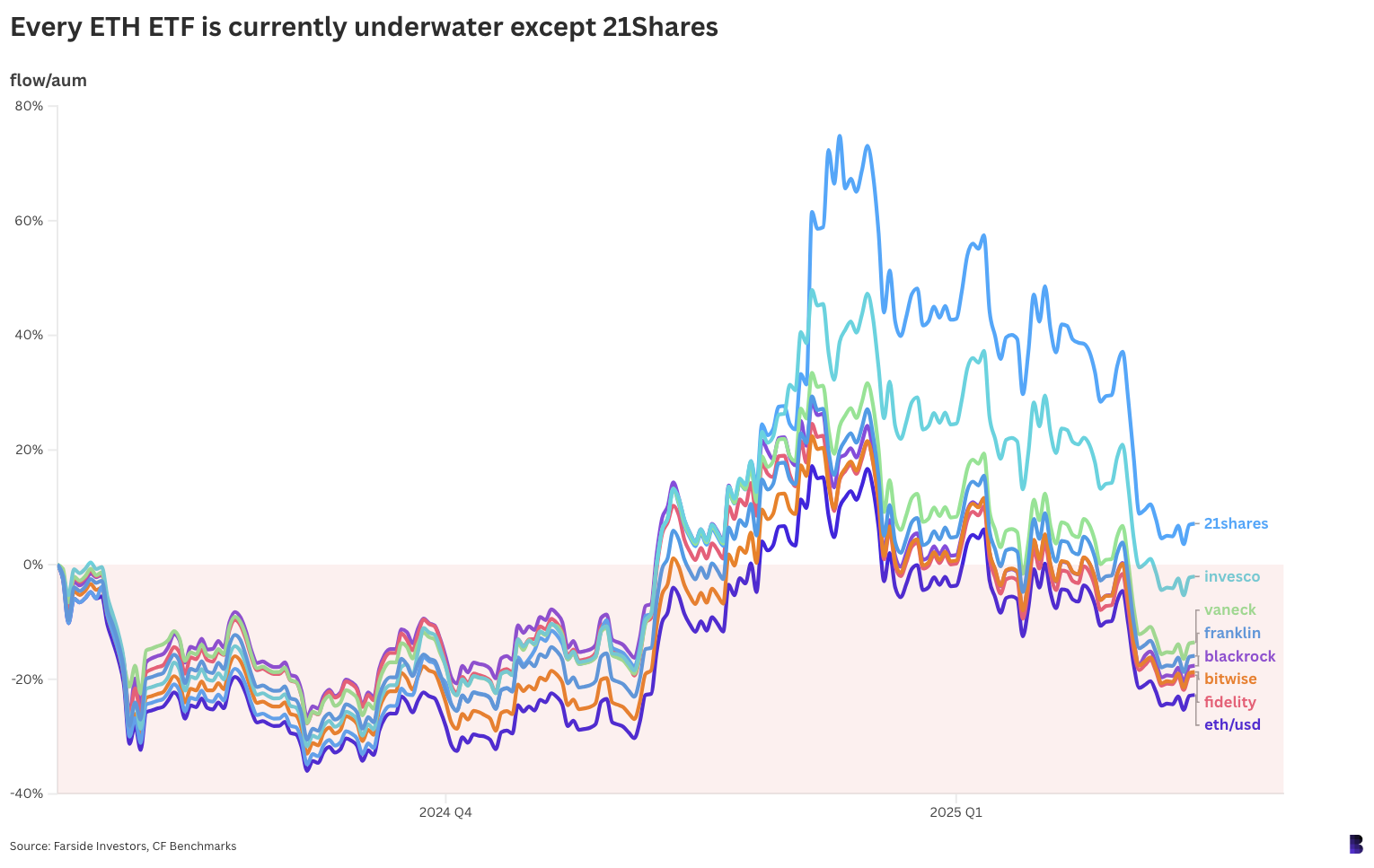

They’re collectively down an estimated $1.16 billion on their capital to date, after contributing the bulk of their inflows when the price of ETH was closer to $3,300, or around 27% higher than it is right now.

To be clear, the share prices of the ETFs themselves more-or-less track the price of ETH. The losses referred to here point to the ETH value each fund holds compared to how much was spent acquiring it.

How to calculate: Take the daily US dollar flows for each ETF and divide them by the daily reference rate. This gives a rough outline of how many ETH units the ETFs buy and sell every trading day.

Then, tally those ETH units and multiply the total by the price of ETH — that will give the current value of each fund’s ETH holdings, which technically belong to their respective shareholders.

Divide the current value of each fund’s ETH by the total amount of US dollars that have flowed into each one to date, and you’ll get a reading on how well each fund has actually performed for its shareholders so far.

Each line shows the performance of each fund. The blue line at the bottom plots the price of ETH

(Grayscale’s ETFs weren’t included in this analysis as most of their capital flows occurred long ago, so their performance isn’t easily calculable.)

As it turns out, 21Shares’ CETH, in light blue, is the only ETF ahead on its net flows.

CETH is currently holding about $18.11 million in ETH, while its total cumulative net flows were only $16.9 million — putting it $1.21 million in the green, or nearly 7.2%.

Fidelity’s FETH is the worst performer of the bunch. It’s sitting on $1.21 billion in ETH from almost $1.5 billion in net flows, so it’s down $289.2 million or just under 20%.

BlackRock’s ETHA is otherwise down 17.6%, which is slightly better performance based on percentages, but due to the size of the fund it has lost its shareholders more dollars than any other — the equivalent of $782.5 million.

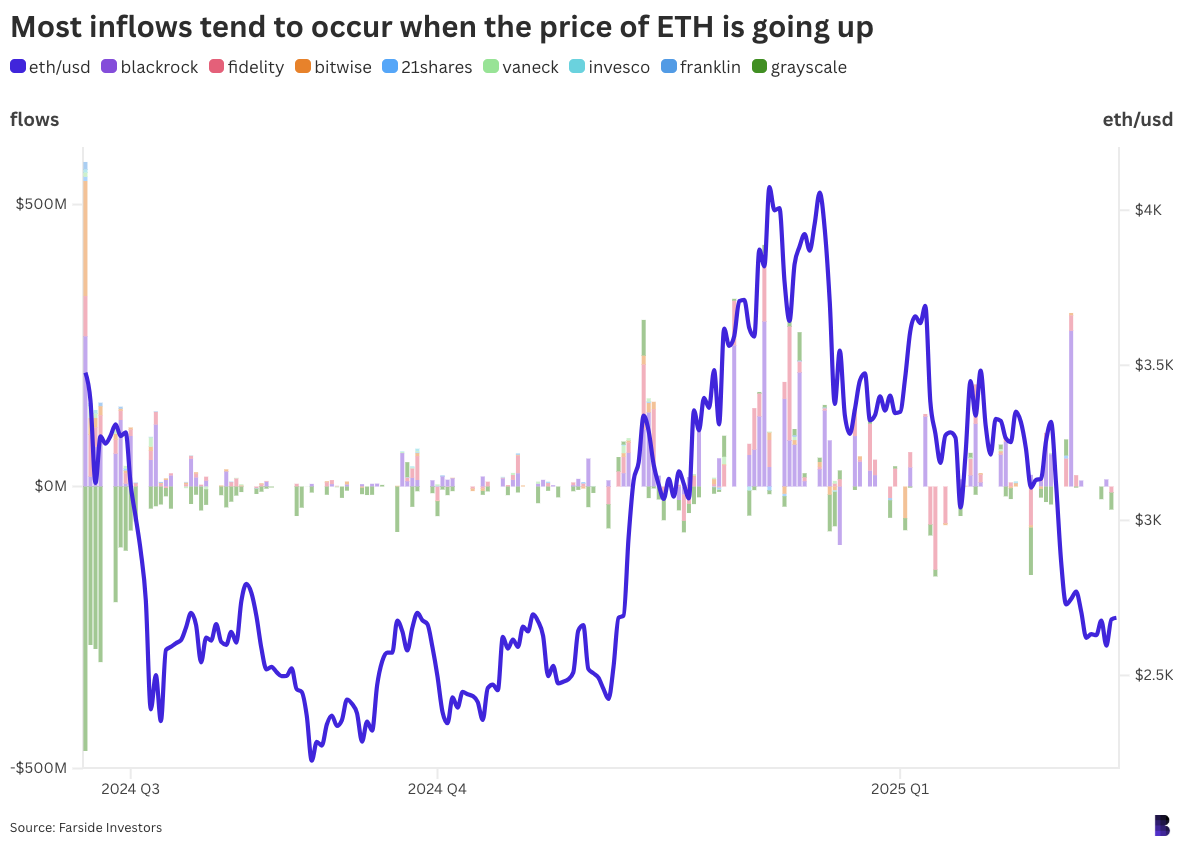

The strategy is buy low and sell high. But ETF customers haven’t quite nailed that yet. Net daily flows are the columns in the background, the blue line is the price of ETH.

Why are some funds performing better than others? Simple: it depends on when ETF customers contribute and withdraw their capital.

Take 21Shares’ CETH. Most of its inflows to date occurred between September and November last year, when ETH had traded for well under $2,500 at times.

Then, CETH customers redeemed $15 million worth of shares between November and December, when ETH had rallied by around 60% from local lows to briefly clear $4,000. Literally, CETH holders had bought low and sold high.

In any case, a clear cure-all would be for the price of ETH to go up. Vitalik’s recent tweet about “making communism great again” hasn’t gone over well — might I suggest posting almost exclusively about the roadmap, as that seems to do the trick.

— David

P.S. Help us build a better Empire and complete our short audience survey. Thank you!

Six weeks until DAS NYC.

Big names. Big conversations. Big moves.

Mohamed El-Erian on the macro forces shaping global markets.

Mike Novogratz on where institutional capital is actually flowing.

Anatoly Yakovenko on the tech pushing crypto and finance forward.

Bring your team. Group passes are 25% off for 10+ people, but only until Feb. 14. Smaller groups (4-9) still save 15%.

📅 March 18-20 | NYC

Tether might have to hit the sell button on some of its non-compliant assets, like bitcoin, in order to comply with the proposed stablecoin regulation in the US.

On the other hand, if the state-level bitcoin reserve bills are enacted, the states could then buy up $23 billion of bitcoin according to VanEck’s Matthew Sigel.

The party’s just getting started: Robinhood reported a stellar quarter thanks, in large part, to crypto.

✅ Vibe check

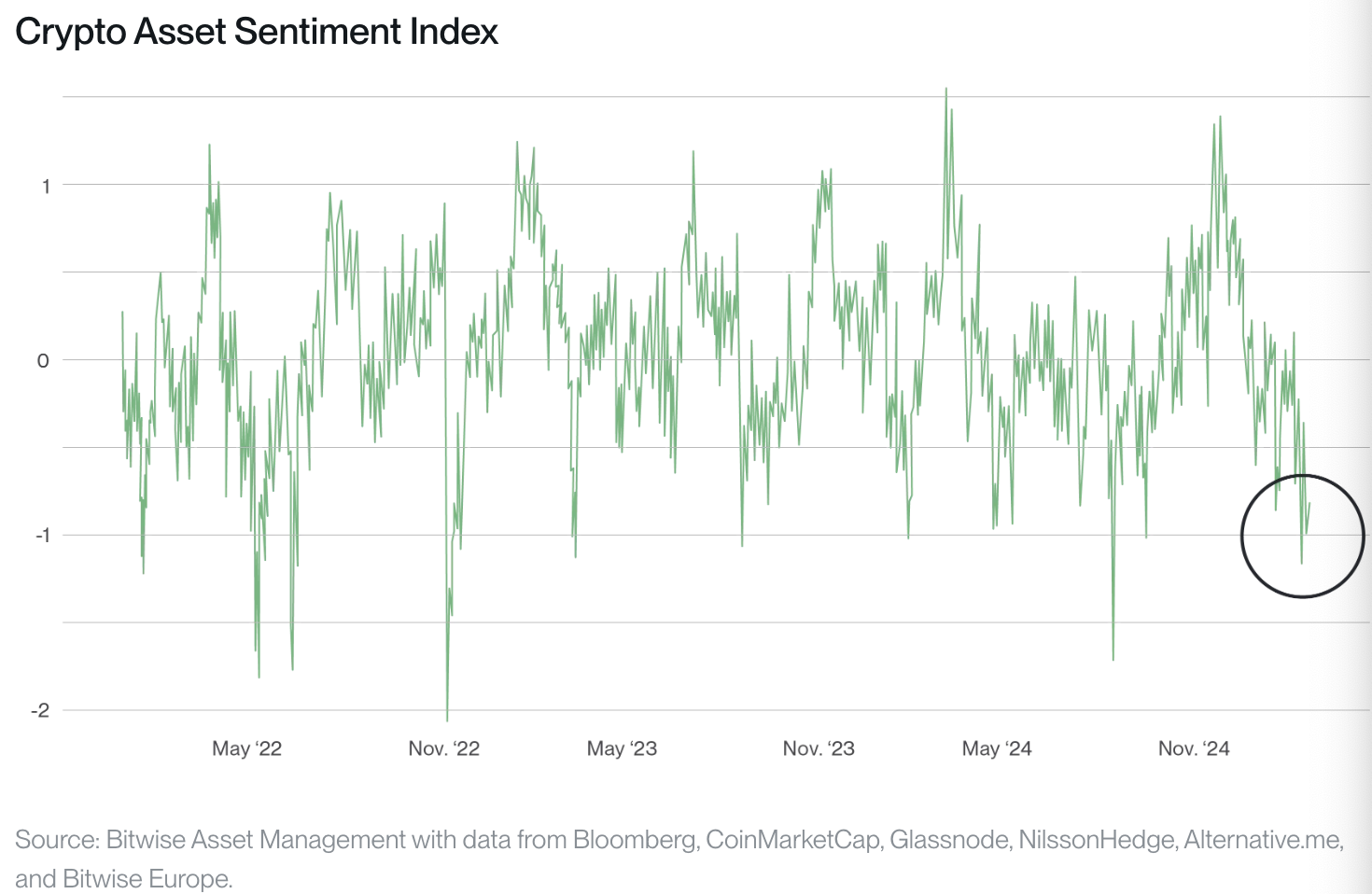

I’m going to be honest with y’all: I’ve been down bad with the flu this week. But from where I’m sitting, CT’s vibes are still off.

And, unfortunately, Bitwise’s crypto asset sentiment index is echoing the same vibes we’ve picked up on.

Everyone’s left wondering — unless you’re David — where altcoin season is and if it’s even possible at this point. (If you didn’t read yesterday’s Empire, then you’re in for a somewhat optimistic surprise about altcoin season’s potential.)

Is this potentially a sign that we’re still early in the cycle? Perhaps, given that historically altcoin season comes at the tail end of the bull market, but we can’t ignore that things are different this time around.

For Bybit, one potential difference is the institutional entry because they’ve changed the way that capital has traditionally flown. And, to add to that, Bitwise’s Matt Hougan said that the institutional sentiment in crypto is “the most bullish I’ve ever seen.”

But those institutional investors? They’re not going to swap out their bitcoin holdings for altcoins even with a friendlier regulatory environment, which could explain some of the down bad energy we’re seeing.

Though Bybit’s not willing to throw in the towel just yet, with analysts noting that “robust stablecoin supply growth and record exchange volumes point to ongoing retail engagement, suggesting that while the script may have changed, an altseason-like frenzy could yet materialize if the right confluence of events aligns.”

This could be likely, especially when looking at Robinhood’s earnings from last night. Revenue from crypto trading in its last quarter surged 700%.

I obviously have to caveat that this data is from the prior quarter before we saw the market selloff, but I don’t think that actually makes a huge difference here.

The point remains that retail has come running back.

Vibes are one thing, but data is another and I’m more inclined to lean into the data personally.

— Katherine

On our mind: Founder energy

Katherine: One of the surefire ways to change the vibes is through positivity. Right now, I think it’s actually important for public-facing founders and even influencers to be positive about things they’re genuinely excited about (but please, for the love of crypto, do not fake the vibes). In my conversations with folks, there seems to be a lot of chill yet happy energy, and yet places like CT seem like desolate wastelands by comparison. I just think we could all push a bit more positivity in the space. | David: Surely one of the cruelest quirks of the crypto space is the necessity for founders to double (or even triple) as reply guys and influencers. Cross that with recent cringes — such as Solana co-founder Anatoly not regularly using the Solana blockchain, or Binance co-founder CZ not knowing how memecoins are created or promoted — and it’s clear that perceptions of individuals in the space don’t always line up with reality. So, should all founders be super shadowy coders who only ever tweet anonymously or pseudonymously? Probably not. But I can’t help but think we could do with a little more of it. |